cl update

2009 ANNUAL CONTACT LENS UPDATE

Despite a cloudy year, our annual report reveals several rays of light.

RICHARD MARK KIRKNER, Phoenixville, Pa.

Although patient visits for contact lens (CL) wear declined about 5% in 2008 from 2007, the CL market continued to see areas of growth and an extension of certain trends, revealing its strength in challenging times.

This data comes from Health Products Research (HPR), an in-Ventiv Health Company in Somerset, N.J., that conducts marketing research and analysis for the medical-products, biotechnology and pharmaceutical industries. In this case, HPR gathers surveys from optometrists, ophthalmologists and retail eyecare locations, and tallies their reported patient visits for CL care to analyze trends and calculate market share at the manufacturer and brand levels.

Data for 2008 revealed these findings:

SiHy visits grew

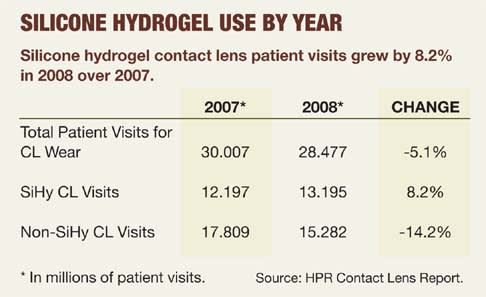

As CL data has shown for the past few years now, patient visits for silicone hydrogel (SiHy) CLs once again increased. Specifically, total patient visits for silicone hydrogel (SiHy) CLs grew 8.2% from 2007 to 2008. Although this number is considerably less than the 23% year-over-year increase this category showed in 2007, considering that the overall market contracted by 5.1%, this is a real sign of vigor for this CL category. (See "Silicone Hydrogel Use By Year," below.)

"The trend for the last five years is that an increasingly higher proportion of patient visits are for SiHy lenses," says Molly Thompson, an associate director of client solutions at HPR who tracks the data monthly and regularly converses with CL companies. In fact, 46% of patient visits were for SiHy CLs in 2008.

Greg DeNaeyer, O.D., a CL specialist in Columbus, Ohio, credits SiHy CLs for a "paradigm shift" in CL fitting. "The silicone hydrogels have increased oxygen permeability, which we [optometrists] think is healthier for the cornea," he says. "What's definitely been proven is that they are not any safer for continuous wear, but what we found out — which nobody anticipated — is that after fitting these lenses, SiHy [CLs] are significantly more comfortable for patients who are dry."

Daily wear schedule increased

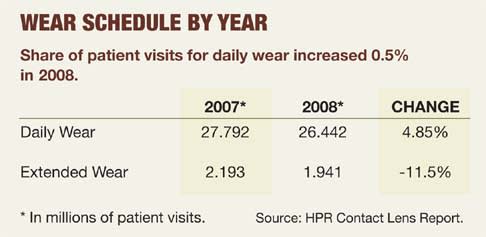

In 2008, patient visits for extended wear schedule CLs declined about 11%, while patient visits for daily wear schedule CLs grew almost 5% — a trend continued from the 2007 HPR data. (See "Wear Schedule By Year," below.)

"A lot of us will prescribe a daily wear [CL] just for safety issues," says optometrist Pam Miller of Highland, Calif. "I personally have never been a fan of extended wear lenses, and when I have had patients who wear their lenses extended wear, it typically will be a three-night maximum [situation], and I will explain why." The side effects of early extended wear in the 1970s never left her memory, she says.

Optometrist Susan Kovacich, an assistant professor at the Indiana University School of Optometry, says her practice bucks this trend, as she sees a lot of college students. "Patients want to not have to fiddle with their lenses, especially if they're in college," she says. "Improved SiHy materials actually make continuous wear an acceptable option for these patients."

Shorter modalities rose

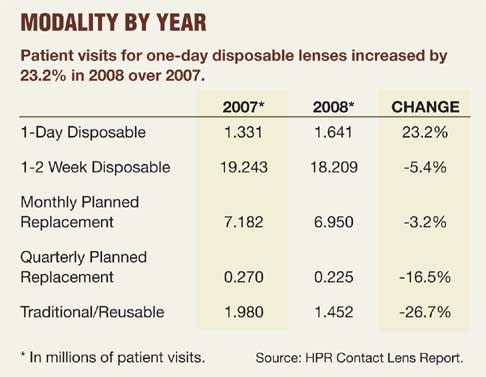

HPR data revealed that patients in 2008 continued moving from traditional and quarterly replacement schedules into shorter replacement schedules. Weekly or bi-weekly disposables held the lion's share of patient visits — around 64% — just slightly lower than in 2007. Almost a quarter of all patient visits in 2008 were for monthly planned replacement lenses, a slight increase compared with 2007.

Patient visits for the one-day disposable modality increased by 23.2% over the previous year, now comprising 6% of overall patient visits. A similar strong growth rate was seen in 2007. (See "Modality By Year," below.)

"I think there are three reasons for this continuing growth. First, I think we're playing catch up with the European and Asian markets, which fit more one-day disposable lenses than we do and by a large margin," says Dr. DeNaeyer. "Second, I think practitioners are realizing that people intolerant to contact lens wear as a result of dryness or allergies are able to achieve success with one-day daily disposables and as a result, are offering them to these patients. Finally, I think practitioners have been successful in marketing these lenses to part-time wearers, who, due to their part-time wear, don't want to get involved with solutions."

The loyalists: astigmatic and presbyopic patients

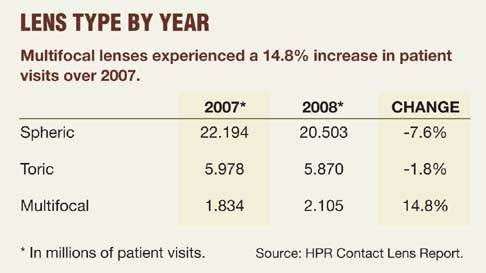

The more demanding a patient's vision needs, the more loyal the patient — or so HPR's data indicated. Actual patient visits for toric lenses declined 1.8% in 2008, but this decline was less than that for spherical lenses. Patient visits for multifocal CLs reflected a net gain over 2007 of almost 15%. (See "Lens Type By Year," below).

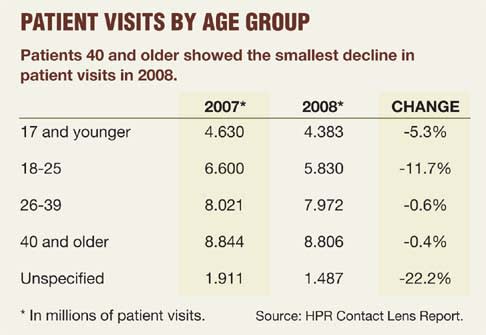

The strong growth in multifocal CLs also seems to be reflected in the age-specific data breakdowns: Although all age groups showed a decline in actual patient visits, those among patients age 40 and older declined only 0.4%. (See "Patient Visits By Age Group," below.)

Ms. Thompson posits that the economy may be affecting 18- to 25-year-old patients, disproportionately — patient visits for this group declined nearly 12% — whereas technological developments may be sustaining fits for toric lenses and driving increased CL patient volume for multifocal lenses.

Optometrist Milton M. Hom, a private practitioner in Azusa, Calif., concurs. "Multifocals are a growing segment of the practice," he says. " … Torics are growing because of the increased modalities, such as silicone hydrogels and the use of low cylinders (-0.75 cyl)."

Dr. DeNaeyer says that improved bifocal soft lens designs have been a lure for presbyopes in his practice. "In the last couple of years, some of the newer multifocal designs have been very successful, and because of that and the aging population, multifocal is a niche design that has the potential to increase volume," he says. (See "Specialty CL Fits Held Their Own," below.)

| Specialty CL Fits Held Their Own |

|---|

| While patient visits for RGP lenses declined to 3.3% of all CL patient visits, specialty products continued to thrive. The following represents a sampling of 2008 results from specialty CL manufacturers. Unilens Vision Inc. reported sales increased 3.3% in the second half of 2008 despite a weakening economy. Unilens chief executive officer (CEO) Michael J. Pecora attributed his company's gain to "double-digit growth" of the C-Vue brand disposable specialty CL sold only to eyecare professionals. Blanchard Contact Lenses Inc. also saw growth. "It wasn't up as dramatically as it was in ’07, but nevertheless we experienced growth," says Lee M. Buffalo, director of sales and marketing. Mr. Buffalo traces much of that growth to the company's Rose K2 IC, an intralimbal design for irregular corneas. "We saw accompanying increases for need in post-refractive specialty lens designs," he says. Art Optical experienced a growth in sales as well and attributes this growth to several product introductions and enhancements. "We entered the custom soft lens arena in July of 2008 with our Intelliwave Precise Prescription product line, and having multiple options for the growing prespyopic population has been very beneficial for us," says Mindy Spicer, the company's director of marketing and communications. ". . .We're able to present the practitioner with a completely customized solution for each patient. When it comes to unique presbyopic prescriptions, we have the opportunity to provide a soft multifocal, a soft multifocal toric, or one of several GP options. As a result of our fuller range of fitting options, we're increasing our practitioner and patient base in the presbyopic segment." SpecialEyes, a made-to-order soft CL company, experienced continued increases between 2007 and 2008. "The patients indicated for our products [have] high cylinder, flat or steep corneas," says SpecialEyes president Steve Brauner. "Many of the eyecare providers we speak to indicate they are seeking a dependable and efficient source to serve this patient population." SynergEyes, a hybrid lens company, had revenues just slightly less than their doubled revenue from 2006 to 2007, says Kellie Kaseburg, SynergEyes vice president of marketing. The SynergEyes Multifocal and the SynergEyes PS lenses, which the company launched in 2008, significantly contributed to the increase in sales in 2008, she says. In addition, sales of the SynergEyes KC lens increased by 33%, and sales of the SynergEyes A lens increased by 22%. "We have noticed that more practitioners are using hybrid CLs as a mainstream product in their practices for normal cornea patients," Ms. Kaseburg says. "Practitioners are looking for CL options that can truly satisfy the largest patient populations in their practice — patients with astigmatism and patients with presbyopia…" she says. Mark Parker, vice president and general manager of X-Cel Contacts (a Walman Company) says that despite the decline in GP CL use, the year 2007 to 2008 revealed a need for more keratoconus and multifocal CLs. "As a company, we sell more GPs than custom soft CLs, however our custom soft CL businesses (Flexlens and Westcon) are the fastest growing part of our specialty business," he says. "In the custom soft category, we see tremendous growth in three areas: unique parameter torics, spheres and again a soft kerataconus design that we sell in our Flexlens line." Paragon Vision Sciences saw demand for its corneal refractive therapy (CRT) products grow 15% in 2008. "Practitioners have begun to focus on two primary markets with CRT: the tween/teen market or, as we like to say, the ‘8-to-18-year-old’ segment, and soft CL wearers experiencing eye discomfort or eye dryness,’" says the company's president and CEO Joe Sicari. GMA-HEMA CL products led a 7% increase in sales for Hydrogel Vision Corporation in 2008. "I think we were getting some positive impact from the new products we launched the year before," CEO Steve Schuster says. "We launched the Extreme H2O Toric in ’07, and I think we were getting a nice uptick from the new toric." Kevin Lippert, president/chief executive officer of Lensco, which recently released the Zenith RG (reverse geometry) GP lens, says the company experienced modest sales growth and are pleased with the results, considering the economy. "Specialty GP CLs have seen a good resurgence in the market," he says. "Lenses for keratoconus, multifocal [CLs] and large diameter CLs have dominated the GP segment…" Menicon Company, Ltd. grew its global business in 2008 by 4.4% vs. the prior year. Its primary driver of growth outside Japan: specialty GP CLs and the introduction of the PremiO two-week silicone hydrogel CL in selected markets, says Jonathan Jacobson, Menicon's general manager, Global Strategy and Operations. "There is clearly a trend to fitting more hyper-Dk specialty CLs around the world. Practitioners are seeing the value and benefits of fitting hyper-Dk CLs on their GP patients," he says. "Another growing trend is the use of software-based fitting systems using topographical data for the fitting of GP CLs…" Marietta Vision reports sales of its prosthetic lenses continued to grow, that business for its VisionCare Toric (formerly the Definition AC toric) nearly doubled in one year and its custom "sport tint" CL line saw a 30% growth. "We have noticed a greater demand for high technology and custom CL items. Our practitioners like using products above and beyond what is found in the ‘big box’ optical stores that also sell groceries," says John M. Patterson, Marietta Vision president. "We are selling custom sport tint toric CLs every day. We didn't see that demand two years ago. Just last year, the only industry talk was about silicone hydrogel CLs. That is no longer the case." Essilor says its GP CL division continued to show solid growth, with the specialty categories of multifocal, post-surgical, keratoconus, astigmatic, ortho-K and scleral CLs driving sales. "During the challenging economic times, practitioners are seeking ways to optimize their practices by taking very difficult fittings, which might have previously been referred elsewhere," says Jeff Duncan, Essilor's director of Prescription Safety Eyewear & Contact Lenses. "This is providing us the opportunity to expand our customer base to a larger number of specialty fitters." The bottom line So, how can you capitalize on this information? "The first step is to take time to learn how to fit a few new CL designs… It's crucial to understand these designs and their applications before beginning the fitting process…" says optometrist Dianne Anderson, who performs a number of specialty fits in Aurora, Ill. "The next step is to fit a few loyal patients who are good candidates for these CL designs. And take advantage of the expert consultation available from the CL manufacturers. A slow but good start is the way to build a fast-growing specialty CL practice. When you achieve success with these new designs, you can advertise with in-office brochures and Web site updates. Patients are very receptive to new CL product offers." |

Tips for growth

Now, that you know where the growth areas were in 2008, here are some tips on how to capitalize on this data in your own practice.

► Educate patients about the importance of complying with regular exams. "To give yourself an excellent chance of achieving compliance with regular exams, educate patients that because their ocular needs and prescriptions may change, stockpiling CLs isn't a good idea," says Dr.Miller. "This instills in them the importance of regular exams, which should increase your patient visits for CLs. We reinforce continuation of care by pre-appointing all our patients, allowing us to monitor our patients' needs and health."

► Encourage the SiHy CL switch. "Educate HEMA patients whose parameters are available in SiHy CLs that you have the ability to fit them in a lens that transmits more oxygen, which is healthier for their cornea," says Dr. Kovacich. "Even if the patient's eyes look healthy, always present this option. If he hears about SiHy technology elsewhere, you risk losing the patient, regardless of whether he's interested in making the switch."

► Explain to patients the significance of wear schedules. "Educate the patient that the modality you've prescribed is constructed of a material that requires adherence to the wear schedule and that by not adhering to the schedule, he puts himself at risk for infection," says optometrist Thomas G. Quinn, of Athens, Ohio. "You want to explain that two-week replacement lenses, for instance, do not have the level of deposit resistance needed to wear them longer than two-weeks."

► Promote one-day disposable CLs. "Ask patients about their lifestyle to see whether they could benefit from these lenses, and educate them that they won't need lens care solutions, as they'll be placing a fresh lens on their eye every day," says Dr. DeNaeyer. "Some practitioners have been reluctant to market these lenses because of their cost differential from other lenses. If you're one of these practitioners, realize that cost isn't always a barrier to patients, such as sports enthusiasts, who understand and appreciate the benefits these lenses offer."

► Offer multifocal CLs to all your presbyopic patients. "Ask your presbyopic patients whether they'd like to see well both in the distance and near without spectacles. Most will say they would. If the patient is wearing monovision contact lenses, ask him whether he'd like to have better distance vision. Again, most would say they would," says Dr. Hom. "Also, keep in mind that anyone who's wearing an older multifocal contact lens is perfect for the newer multifocals. It's a no brainer. The success rate for this lens is just off the charts."

► Embrace the new toric lens designs. "The toric designs have significantly improved over the last few years, so give them a try, and particularly on those patients who were unsuccessful in the older designs," says Dr. DeNaeyer. "Educate these patients that they may not experience the problems of the past with the new designs because of better technology. And, offer these lenses to patients you previously thought you'd never fit. These lenses don't just improve these patients quality of life, they also offer higher fitting and material fees."

While 2008 may have been the beginning of doom and gloom for several markets as the result of the economic downturn, the CL market managed to grow in several areas, as HPR-reported patient visits revealed. This is a huge ray of light for you, the eyecare practitioner. Now, it's up to you to use this data to increase your patient visits for CLs and increase revenue for 2009. OM

If you would like to become a participant in HPR's Vision Care panel, please visit www.rxsurvey.com/enroll.

| Mr. Kirkner is a medical editor and writer in suburban Philadelphia. |

A Wall-Street Perspective

Silicone hydrogel and daily disposable lens sales continue to grow despite the economy.

JEFFREY D. JOHNSON, O.D., C.F.A.

When the economy goes south, wallets and pocket books slam shut, testing the strength of several markets. This began to occur between 2007 and 2008 with the credit crisis. Although the contact lens (CL) market was not immune, it revealed itself as resilient with continued increases in sales.

Based on publicly available data and industry sources who closely follow the CL market in the United States and abroad, my colleagues and I estimate that the U.S. CL market grew roughly 4% to 5% between 2007 and 2008 at the manufacturer level. Through the first nine months of 2008, the domestic CL market actually grew closer to 6%. But with sales decreasing nearly 10% in October (a period of time when the whole world seemed to shut down and the severity of the worldwide credit crisis was fully realized) and rising 2% to 3% in the combined November/December period, growth for the full year fell to 4% to 5% — approximately two points below the 6% domestic market growth recorded in 2007.

Worldwide, CL sales grew approximately 7% to 8% between 2007 and 2008 to nearly $5.2 billion. At least several points of this growth were due to the weak U.S. dollar. (A weak U.S. dollar adds to sales totals for U.S.-based manufacturers when sales in foreign currencies, such as the Euro and Yen, are translated back into U.S. dollars).

Excluding the impact of currency movements, my colleagues and I estimate the worldwide CL market likely grew roughly 4% to 5% between 2007 and 2008 — in line with the United States — but one to two points below last year's worldwide constant currency market growth.

Using the same publicly available data and CL industry contacts, the year 2007 to 2008 revealed daily disposable and |silicone hydrogel (SiHy) lenses as the primary growth drivers both in the United States and Worldwide.

Daily disposable use increased

Outside the United States, daily disposable CLs accounted for a little more than one-third of soft CL sales, according to our estimates. Use of this modality is highest in countries such as Japan, Hong Kong, the United Kingdom, Norway and Denmark (40% to 50% plus market penetration in these countries, according to independent industry sources). Why? Different fitting philosophies exist in a number of these markets, while more meticulous attention to hygiene and greater concern about CL-disinfecting — especially in warmer climates — also play a role.

Overall, we believe the daily disposable CL category likely grew 10% or slightly higher in 2008 on a worldwide basis — a nice premium to the 7% to 8% we estimate the total worldwide CL market grew for the year 2007 to 2008.

Daily disposable CL use in the United States continued to grow rapidly for the year 2007 to 2008, with sales increasing roughly 20% in 2008 to more than $200 million (at the manufacturer level), according to our estimates.

In fact, my colleagues and I estimate that daily disposable CLs now account for nearly 12% of the U.S. CL market — up from 10% in 2007 — continuing what has now been a threeyear trend of gaining one- to two points of market share annually. The reasons my colleagues and I believe daily disposable CL use has picked up in the United States in recent years:

► The highly publicized lens care solution recalls in recent years involving both fusarium and acanthamoeba keratitis cases has lingered in the minds of patients, making them leery of the extended-wear option.

► CL manufacturers have begun to offer more competitive price points in the last few years, making this option only slightly more expensive than two-week or monthly disposable options after factoring in CL solution costs.

► CL manufacturers have launched several new daily disposable options through the last few years that provide either improved comfort (through the addition of "moisture retaining" properties) or vision (including both aspheric and toric options), thus expanding the range of patients who can potentially choose this modality.

SiHy CL wear rose

While daily disposable growth in the U.S. likely outpaced that of the SiHy family of spherical, toric and multifocal products for the first time since 2003, we estimate SiHy market growth remained healthy nonetheless, up roughly 15% to 20% in dollars for the year 2007 to 2008.

In all, my colleagues and I believe domestic SiHy CL sales totaled just under $1 billion in 2008 vs. approximately $850 million in 2007.

Interestingly, my colleagues and I began to see a subtle shift away from two-week replacement schedule CLs toward monthly replacement schedule CLs. We believe this is due to the increased recognition on the practitioner's part that poor patient compliance with two-week disposable schedules and higher price points with monthly disposable products can create greater profit potential for the monthly segment of the market. Still, the two-week replacement schedule CL continues to dominate in the U.S. market and will likely continue to do so for the foreseeable future. This is because the two-week replacement schedule CL comprises 60% of the U.S. market, while the monthly replacement schedule CL comprises about 20% of the market.

We estimate the U.S. spherical SiHy lens sales grew roughly 11% to $739 million in 2008, with this lens type accounting for nearly 75% of the entire domestic SiHy CL category during the year.

My colleagues and I believe toric SiHy CL sales in the United States increased approximately 40% to $225 million between 2007 and 2008, with nearly 50% of domestic toric CL revenues now coming from SiHy products vs. less than 10% in 2005. The reasons for this rapid movement? We believe greater understanding and willingness to use SiHy products on the part of doctors has combined with high-quality products launched from the leading CL manufacturers in recent years to drive this rapid adoption.

U.S. sales of multifocal SiHy CLs rose roughly 30% to nearly $30 million in 2008. We believe this growth is due to the prevalence of baby boomers and improvements in technology.

We estimate that the penetration rates for SiHy products across all categories increased to just under 50% between 2007 and 2008 in the U.S. vs. nearly 45% last year. My colleagues and I believe the reasons for this growing penetration include:

1. Improved oxygen transmissibility, and, thus, reduced hypoxia-related stress to the cornea.

2. Anecdotal reports of improved comfort (especially at end of day) vs. standard hydrogel lenses.

3. Higher price points at which these CLs sell, which we believe contributes to the increased marketing focus both the practitioner, and CL manufacturers place on these lenses vs. standard hydrogel lenses.

Outside the U.S. market, SiHy CL use varies widely, making market size difficult to estimate. Still, independent market research suggests that the SiHy CL penetration rates in Canada, Australia and New Zealand are similar to those seen in the United States. Meanwhile, market data reveal that practitioners in Japan, Hong Kong, Germany and Spain continued to fit fewer patients in SiHy CLs, given their preference for daily disposable CLs.

Predictions

Because of the current state of the economy, predicting future growth and trends for the year 2008 to 2009 is extremely difficult. But, if my colleagues and I were forced to venture a best guess at this point, we'd feel comfortable assuming domestic market growth in 2009 will potentially land somewhere between the 5% to 6% range seen during all of 2008 and the flat-to-down 1% range seen through the final three months of 2008.

This suggests U.S. market growth in the 2% to 3% range for the year 2008 to 2009. We base these predictions on the following:

► Slower growth is expected to largely result from the current mounting job losses in the United States, which translates to fewer insured patients showing up for exams and potentially into consumers who might decide to stretch the life of their lenses beyond their prescribed disposal schedule.

► Offsetting these pressures, we believe the market can still grow slightly as pricing has remained rational and relatively flat to up slightly across the industry in recent years and as CL manufacturers plan several product launches for this year (See "In The Pipeline," below.)

| In The Pipeline |

|---|

| Based on information from various industry insiders, here are the new product launches currently in the works for 2009: ■ CooperVision will launch a monthly toric SiHy lens under the Biofinity brand name during Q1-09. ■ Vistakon will release an Acuvue Oasys multifocal lens and its one-day Acuvue TrueEye daily disposable lens (currently available in Europe) in the U.S. in May. ■ CIBA Vision may launch a SiHy multifocal. |

Considering so many other markets are fighting for survival, my colleagues and I believe the resiliency of the CL market is a testament to currently available products. In other words, we believe that if a patient likes his CLs, and he doesn't want to have to wear spectacles, he'll keep buying them regardless of the state of the economy. Consumers place a great deal of value on products that improve their quality of life, and CLs are one of those products. We believe this has insulated the CL market a bit when compared with other markets.

Although in the past, several wearers have obtained their lenses from retailers, as opposed to their practitioners, a weak economy encourages even more of this behavior. As a result, it's more important than ever that optometric practices distinguish themselves from CL retailers to increase the likelihood of CL purchases at the practice.

"You need to communicate to the patient the benefits of obtaining their lenses from you instead of from the retailers. These benefits include convenience — since the patient is already at your practice — personalized service and competitive pricing," says optometrist Thomas G. Quinn, of Athens Ohio. "We have a handout we give to all our contact lens patients that briefly outlines why they should get their supply from us, and I'm happy to say it's enabled us to garner healthy sales." OM

| Dr. Johnson is a vice president and the senior medical technology research analyst covering orthopedic, ophthalmic, dental and radiation oncology stocks at Robert W. Baird & Co., in Milwaukee. |